The Wall Street Journal/Realtor.com Emerging Housing Markets Index

Introduction

As temperatures drop, the housing market tends to follow suit, cooling from summer’s fever into winter’s freeze while home shoppers shift their attention to the season’s festivities. After a sluggish summer market due to widespread unaffordability, the fall is shaping up to offer little relief. Mortgage rates hit a more than two-decade high in October, climbing to 7.57% as home prices also rose compared to the previous year.

Home shoppers are facing not only higher housing costs, but also dwindling home supply. Many homeowners hold a mortgage loan at a lower rate than today’s, making them hesitant to sell. As a result, for-sale inventory has fallen and existing home sales have stalled as the mismatch of buyer demand and for-sale inventory constrain the market. New construction served as a welcomed alternative through the summer, but climbing mortgage rates impacted both buyer activity and builder sentiment, and new home sales dropped 8.7% in August.

September’s CPI inflation data showed steady headline inflation, but continued progress in core inflation, a welcomed, though not overtly strong, sign that the Fed’s contractionary policy is having the intended effect. Though the latest data is moving in the right direction, the long and tedious road to 2% inflation is not yet over. The Fed signaled in their latest meeting that rates are likely to be ‘higher for longer’ than previously projected, which keeps upward pressure on mortgage rates as investors adjust their expectations. Employment activity picked up more than expected in September, adding 336,000 jobs throughout the month, a jump compared to recent months, adding to investor anxiety around the Fed’s path forward. Unemployment ticked up slightly to 3.8% in recent months, but remains low, meaning that consumers remain in a stable position to weigh housing decisions.

The fall’s market may usher in the winter housing freeze earlier than is typical, as buyers faced with high housing costs choose to opt out of the market altogether. However, even amid mounting affordability challenges, the tension between low buyer demand and perhaps even lower seller activity is keeping upward pressure on prices. After mild declines this summer, the national median listing price has crept back above previous-year levels over the last two months and registered 40% higher than pre-pandemic levels in September. Homes spent one day longer on the market than the previous year in September, but time on market remained two weeks shorter than pre-pandemic. Though housing activity has slowed nationally, demand in affordable locales keeps inventory conditions tight, price growth strong, and time on market snappy. Buyers continue to zone in on affordable areas as emphasized in previous Emerging Housing Markets Index releases.

Fall 2023 Top 20 Emerging Housing Markets

Today’s home shoppers are faced with elevated inflation, scarce home inventory, and still high home prices, making homebuying a challenging feat. The Wall Street Journal/Realtor.com Emerging Housing Markets Index highlights housing markets that offer shoppers a lower cost of living, including for homes, and thriving local economies that are attractive, but not too crowded. The index identifies markets that those considering a home purchase should add to their shortlist–whether the goal is to live in it or rent it as a home to others.

We reviewed data for the largest 300 metropolitan areas in the United States. The Fall 2023 ranking surfaced the following top areas:

| Rank | Metro | Population | Unemployment Rate (%) | Median Home Listing Price September 2023 |

| 1 | Topeka, Kan. | 231,783 | 2.9% | $250,000 |

| 2 | Elkhart-Goshen, Ind. | 206,890 | 4.3% | $280,000 |

| 3 | Oshkosh-Neenah, Wis. | 170,718 | 2.5% | $317,000 |

| 4 | Fort Wayne, Ind. | 426,076 | 3.3% | $312,000 |

| 5 | Lafayette-West Lafayette, Ind. | 226,452 | 3.2% | $293,000 |

| 6 | Racine, Wis. | 195,846 | 3.4% | $352,000 |

| 7 | Manchester-Nashua, N.H. | 426,594 | 1.7% | $535,000 |

| 8 | Concord, N.H. | 156,020 | 2.1% | $550,000 |

| 9 | Columbus, Ohio | 2,161,511 | 3.1% | $380,000 |

| 10 | Johnson City, Tenn. | 210,256 | 3.4% | $425,000 |

| 11 | Kingsport-Bristol-Bristol, Tenn.-Va. | 311,272 | 3.3% | $325,000 |

| 12 | Jefferson City, Mo. | 150,350 | 2.5% | $318,000 |

| 13 | Springfield, Ohio | 134,831 | 3.5% | $200,000 |

| 14 | Santa Maria-Santa Barbara, Calif. | 443,837 | 4.0% | $1,895,000 |

| 15 | Dayton, Ohio | 812,595 | 3.6% | $240,000 |

| 16 | Janesville-Beloit, Wis. | 164,060 | 3.3% | $320,000 |

| 17 | Canton-Massillon, Ohio | 399,316 | 3.6% | $235,000 |

| 18 | Knoxville, Tenn. | 907,968 | 3.0% | $475,000 |

| 19 | Hartford-West Hartford-East Hartford, Conn. | 1,221,725 | 3.4% | $400,000 |

| 20 | Worcester, Mass.-Conn. | 980,137 | 2.9% | $490,000 |

More For Less

Home listing prices started to climb again annually in August, spurred on by buyer competition for scarce inventory. Though the cost of purchasing a home has stabilized or fallen in some areas, low-priced locales have gained in popularity, leading to accelerating price growth. Despite climbing prices, 15 of the Fall Emerging Housing Markets were lower priced than the national median of $430,000 in September. The housing market has not yet made significant strides towards affordability and as a result, Fall 2023’s emerging markets continue to lean heavily on outright or relative affordability. The lowest priced locale on the list, Springfield, Ohio, offered 54% savings on the median priced home relative to the national level in September.

Though these areas are largely lower-priced, they boast more amenities than the 300 largest metro average. Amenities are measured as the average number of stores per specific “everyday splurge” category (coffee, upscale/specialty grocery, home improvement, fitness) per capita in an area. Buyers are looking to save without compromising on comforts, and this quarters emerging housing markets deliver.

Demand Outpaces Inventory: Price Growth and Dwindling For-Sale Listings

Though buyers are drawn to these areas for low prices and positive quality-of-life metrics, they face low inventory, climbing prices and a quick market pace. The median price of the typical home for sale was just slightly higher than last September nationwide but these top markets continue to see significant price growth both annually and relative to the pre-pandemic timeframe (2017-2019). While the national market has seen prices hover just below or just above last year’s level for the last few months, this quarter’s emerging markets have continued to attract attention due to their affordability and desirability, which has kept price growth strong. Mortgage rates have picked up even more steam since last quarter, putting even more pressure on buyers to lock-in an affordable home.

The average increase in listing price was 19% among the top 20 markets compared to 9.5% nationally for the 12 months ending in September 2023. All of the top markets except Springfield, OH saw price growth exceed the national rate. Compared to pre-pandemic (2017-2019), home prices were 69% higher in Q3 of 2023, while nationally prices climbed 47%.

High demand in the top emerging markets meant that homes sold quickly, preventing the inventory build-up seen nationwide. Inventory increased an average 8% annually in the top 20 markets in the 12 months ending in September, lagging the 34% build up across the 300 largest metros in the same timeframe. Inventory scarcity has kept upward pressure on home prices over the last few years as buyer demand outstripped some supply. Compared to pre-pandemic (2017-2019), the top emerging housing markets saw for-sale inventory fall an average 62%, exceeding the 47% national decline.

Because buyer demand continues to outmatch limited inventory, home prices have climbed, and market pace is quick. On average, homes spent 35 days on the market in Q3 of 2023, almost three weeks less than the same quarter in 2017-2019. Nationally this difference is just 13 days, with homes spending 46 days on the market in Q3 2023.

Mid-sized Markets Gain Popularity

Just five of the twenty markets on this month’s list have a population of over 500,000 people. These mid-sized metros are 46% smaller, on average, than the top 300 US metro areas. These less-congested areas also see commute times 5.4% lower than the nationally average. The largest metros on this quarter’s list are Columbus, Ohio and Hartford-West Hartford-East Hartford, Conn., with populations of 2.2 million and 1.2 million, respectively. Interestingly, these two larger markets along with three other markets on the list (including the number 1 ranked Topeka, Kan.) are state capitols. State government employment growth overtook growth for all employees this summer, boosting the job market conditions in these areas.

These smaller markets are not just desirable for lower prices and quick commutes, they also boast a stronger-than-average job market. On average, the unemployment rate is 3.2% in these markets, 0.4 percentage points lower than the 300-metro average. The US jobs market has continued to hum along, adding an unexpectedly high 336,000 jobs in September. Despite the strong employment activity, the unemployment rate ticked up to 3.8%, making these strong job markets all the more appealing. Only Elkhart-Goshen, Ind. and Canton-Massillon, Ohio have unemployment rates higher than the national rate with 4.3% and 4.0%, respectively.

Larger metros, such as Denver, CO, Seattle, WA, Dallas, TX and Portland, OR are among the list of metros that fell the most in this quarter’s rankings. Looking instead at the markets who climbed the most in this quarter’s rankings, we see the popularity of smaller metros emerge. The biggest climbers within the top 50 emerging housing markets include Jackson, MI, Trenton, NJ, and Monroe, MI, each of which have a population of less than 400,000 people.

Typical wages were roughly on-par with the broader market average. However, buyers in these areas benefit from the lower cost of homeownership and overall lower cost of living. Prices in the top emerging markets on average are less than 94% of the national price level, though four markets have prices that are slightly higher than the national average, with Santa Maria-Santa Barbara, Calif. seeing the highest cost of living.

Home Shoppers are Browsing Out-of-Market to Land in Areas Where People Tend to Come and Stay

This quarter’s top markets see slightly more out-of-metro viewership than was typical in the 300 largest metros in the third quarter, and have seen outsized growth in out-of-metro interest. On average, the top 20 emerging housing markets have seen out-of-metro viewership increase 5% year-over-year, reaching 75% of all viewership. The Boston-adjacent Concord, N.H. saw the largest out-of-metro share at 89.7% of views. Also in the Northeast, Hartford-West Hartford-East Hartford, Conn. saw the largest increase in out-of-metro viewership compared to the previous year, an 11.5 percentage point increase.

The high-priced Santa Maria-Santa Barbara, Calif. attracted a sizable 3.2% of its listing viewership from shoppers outside of the United States, suggesting that international demand is applying pressure to already high prices. International viewership increased 0.3 percentage points year-over-year in Santa Barbara, outpacing the slight increase in international viewership among the top 300 metros. For comparison, the average international viewership share was less than half (1.3%) the viewership share in Santa Barbara.

Overall, this increase in viewership from shoppers outside of the metro area emphasizes buyers’ willingness to search far and wide for affordability. This quarter’s markets saw a larger share of out-of-metro viewership than in the previous quarter, showing the increasing push shoppers feel to seek out affordability as mortgage rate pressure increases.

Continuing on last quarter’s deviation from previous trends, Summer 2023 markets have residents who are, on average, somewhat less mobile than residents in the top 300 markets with the share of those moving just 13.1% compared to 13.6% overall. The most significant exception to this trend is Lafayette-West Lafayette, Ind. where more than 1 in 5 residents live in a different house than one year ago.

City Spotlight: Topeka, Kansas

This month’s highest-ranked emerging market is Topeka, Kan. for the first time in the history of the analysis. Topeka offers home shoppers the amenities of a Capitol city at a more affordable price point. Nearby Kansas City has received plenty of airtime lately for their football team’s biggest fan, but just an hour down the road is historic and affordable Topeka, where home prices were 41% lower than Kansas City in September. Home to the Kansas State Capitol, residents of this area can enjoy historical sites as well as nature at Lake Shawnee or Gage Park.

The Topeka area is home to multiple large employers, ranging from government and healthcare to retail and manufacturing. Topeka is home to the state’s largest Wal-Mart distribution center as well as a Goodyear Tire distribution center. Hill’s Pet Nutrition is also headquartered in the metro. Notably, as the state’s capitol, the area boasts strong government and healthcare sectors as well.

The typical home for sale in Topeka was listed for $250,000 in September, a 42% discount compared to the national median. However, the popularity of the market kept upward pressure on prices, which rose 8.7% year-over-year in September. Though prices remain relatively affordable in Topeka, the median listing price was more than $100,000 higher than its 2019 level in September as buyer competition kept prices climbing. Homes spent 30 days on the market in Topeka in September, almost 10% longer than last year, but still 18 days fewer than was typical nationally. The number of homes for sale grew 37.6% annually in September, but remained more than 50% lower than was typical pre-pandemic (2017-2019).

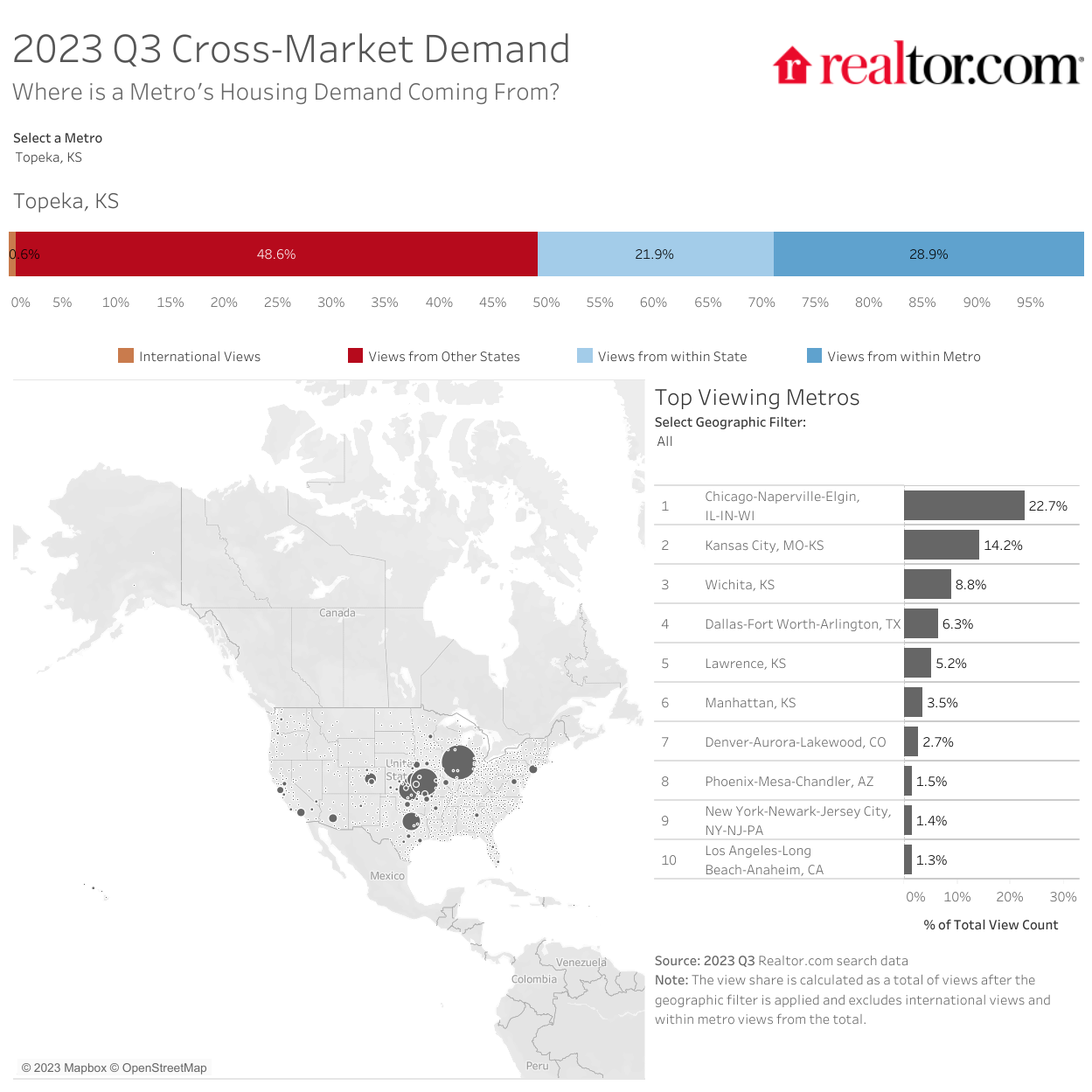

Almost three-quarters (71.1%) of views to properties in Topeka came from outside of the metro in the third quarter, with particularly sizable out-of-metro attention from the Chicago (22.7%) and Kansas City (14.2%) areas. This share increased by 4.1 percentage points in Q3 of 2023 compared to the previous year, indicating a pick up in out-of-metro demand.

Topeka, KS Housing Highlights

| Realtor.com – Topeka, KS: September 2023 Inventory Metrics | ||

| YoY % Change | ||

| Median List Price | $ 250,000 | 8.7% |

| Active Listings | 309 | 37.6% |

| Days on Market | 30 | +3 days |

| New Listings | 268 | -39.4% |

Home Shoppers From Chicago and Other Midwest Metros Drive Topeka Demand

Returning Markets

There are many familiar places on the list of the top 20 emerging markets: 11 members of the Summer 2023 list, including the number 1 market, Topeka, Kan. Among the markets that have remained on our list are the ever-popular southern locales Johnson City, Tenn., and Knoxville, Tenn., as well as the midwestern hotspot of Columbus, Ohio, and various small- to mid-sized midwestern cities that offer affordable housing and low costs of living. Notably, the popular and fast-moving northeastern metro of Manchester-Nashua, N.H. also remained on the list, continuing the reign of Boston metro area locales.

| Market | Fall Rank | Summer Rank | Rank Change |

| Topeka, Kan. | 1 | 7 | 6 spots higher |

| Elkhart-Goshen, Ind. | 2 | 3 | 1 spots higher |

| Oshkosh-Neenah, Wis. | 3 | 17 | 14 spots higher |

| Fort Wayne, Ind. | 4 | 2 | 2 spots lower |

| Lafayette-West Lafayette, Ind. | 5 | 1 | 4 spots lower |

| Manchester-Nashua, N.H. | 7 | 11 | 4 spots higher |

| Columbus, Ohio | 9 | 6 | 3 spots lower |

| Johnson City, Tenn. | 10 | 8 | 2 spots lower |

| Kingsport-Bristol-Bristol, Tenn.-Va. | 11 | 10 | 1 spots lower |

| Jefferson City, Mo. | 12 | 19 | 7 spots higher |

| Knoxville, Tenn. | 18 | 12 | 6 spots lower |

Markets Falling Out of the Top 20

Of the nine markets that did not remain on the list from the summer into the fall, all remained in the top 65. The three biggest movers, Columbia, Mo., La Crosse-Onalaska, Wis.-Minn. and Sioux City, Iowa-Neb.-S.D., which fell 40 spots, 44 spots and 59 spots, respectively, remained near the top fifty, ranking 53rd, 58th and 64th this quarter. The markets that departed the top 20 in our index included two popular Northeast markets, Portland-South Portland, Maine and Norwich-New London, Conn. as well as the midwestern markets of Akron, Ohio, Milwaukee-Waukesha-West Allis, Wis., Bloomington, Ill., and South Bend-Mishawaka, Ind.-Mich. As mortgage rates climbed and kept inventory scarce, these markets were replaced by nearby metros.

New Markets

Taking the places of the 9 descended markets are the five affordable Midwestern locales, plus the three Northeast metros of Concord, N.H., Hartford-West Hartford-East Hartford, Conn. and Worcester, Mass.-Conn. plus the high-priced West coast market Santa Maria-Santa Barbara, Calif. All of the markets except ascended from within the top 60. Much like the markets that stayed in the top 20, the Midwest and Southern new markets were more affordable than the national market, while the Northeast markets were higher priced, but affordable relative to nearby Boston and New York metros. However, the lone West region market is the highest priced market on the list, suggesting that this market’s demand is driven by forces aside from affordability. These newly added markets are on average slightly larger in population than the recently descended markets, though six of the new markets have populations below 500,000.

Methodology

The ranking evaluates the 300 most populous core-based statistical areas, as measured by the U.S. Census Bureau, and defined by March 2020 delineation standards for eight indicators across two broad categories: real estate market (50%) and economic health and quality of life (50%). Each market is ranked on a scale of 0 to 100 according to the category indicators, and the overall index is based on the weighted sum of these rankings. The real estate market category indicators are: real estate demand (16.6%), based on average pageviews per property; real estate supply (16.6%), based on median days on market for real estate listings, median listing price trend (16.6%). The economic and quality of life category indicators are: unemployment (6.25%); wages (6.251%); regional price parities (6.25%); the share of foreign born (6.25%); small businesses (6.25%); amenities (6.25%), measured as the average number of stores per specific “everyday splurge” category (coffee, upscale/specialty grocery, home improvement, fitness) per capita in an area; commute (6.25%); and estimated effective real estate taxes (6.25%).

Read the full article here