Edwin Tan

By Derek Deutsch & Mary Jane McQuillen

Energy Efficiency Has Industrials Humming

Market Overview

The tech-focused rally that dominated the first half of 2023 stalled in the third quarter as a still-hawkish Federal Reserve and higher bond yields weighed on equities and threatened to quell hopes of a soft landing. The benchmark Russell 3000 Index declined 3.25%, with growth and value counterparts declining roughly the same amount.

Most of the turn in sentiment was due to tighter monetary policy beginning to be felt across the economy, as the 10-year U.S. Treasury yield climbed 74 bps during the quarter, reaching its highest level in 16 years. Surging yields have resulted from resilient economic data and a rebound in inflation that caused the Fed to push out any hopes of a rate cut in the near future.

Against this backdrop the Strategy underperformed, with the majority of detractors renewable- or utility-related companies suffering largely from cyclical interest rate pressures that have pushed up financing costs for the companies and weighed on income-producing sectors such as utilities. Most acutely, higher interest rates have dampened near-term U.S. residential solar demand, hurting Enphase Energy (ENPH) in particular. As a result, we sold Enphase, and invested proceeds into SolarEdge Technologies (SEDG), which has greater exposure to European and utility-scale end markets, which are under comparatively less pressure. Shoals Technologies (SHLS), which makes electric balance of systems (EBOS) components, mainly for utility-scale ground-mounted solar projects, was lower in sympathy with other renewable companies.

Utilities NextEra Energy Partners, LP (NEP) and Brookfield Renewable (BEP) have struggled of late due to macro conditions and a general cooling of sentiment and outflows from the clean energy sector as a whole. NextEra cut its growth expectations by half in September, citing higher financing costs, which makes the acquisition of renewable assets less economically attractive. Due to these deteriorating conditions, we exited the remainder of our position in NextEra, which we had trimmed previously. We continue to own Brookfield, which we view as one of the highest-quality pure-play decarbonization investments, characterized by a 5% dividend yield, stable fundamentals (over 90% of its cash flows are contracted with an average term of 14 years), a best-in-class balance sheet and adequate access to capital.

At the same time, an out of favor utilities sector created an opening for us to be opportunistic. During the quarter we added American Water Works (AWK), the largest publicly traded water utility in the U.S., operating across 24 states and providing drinking water, wastewater services and other related services to 14 million customers. Continuous investments in infrastructure improvement, resiliency and water quality should drive solid growth and generate attractive regulated returns for the company for the foreseeable future. In addition, the water infrastructure market remains very fragmented, with 80% of community water systems serving a population of 3,000 or less, enabling American Water Works to continue its strategy of accretive acquisitions to bolster its growth rate.

While renewable stocks have come under pressure of late, energy efficiency and decarbonization remain strong drivers for our industrials holdings, where Eaton (ETN) and Trane Technologies (TT) were strong contributors. Eaton, whose electrical equipment enables the electrification of the power grid and electrical vehicle charging infrastructure, is benefiting from tax incentives supporting clean energy, growth in reshoring and expanding manufacturing in North America and the need for grid resiliency amid broad demand for electrification. Tax incentives to install more energy-efficient equipment are also helping HVAC company Trane, whose products are especially valuable for data centers, which are a large beneficiary of AI investments and require significant cooling.

In a strong showing for the Strategy’s consumer discretionary holdings, Williams-Sonoma (WSM), which sells kitchenware and home furnishings, was the top contributor in the quarter after its August earnings report showed exceptional profitability and the company raised its full-year guidance. Shares jumped further in September after a private equity firm increased its stake, suggesting recent weakness was overdone. The company’s high-quality fundamentals make it a good defensive fit for an uncertain environment: it generates significant free cash flows, has no debt and the liquidity to invest in the business first and then return excess to shareholders.

“The recent Medicare utilization uptick has proved manageable and relatively short term.”

Also in the consumer discretionary sector, Booking Holdings (BKNG) shares rose as travel and leisure companies continued to fare well, with a strong summer season of travel driving positive sentiment. Booking maintains a strong competitive moat, in terms of direct traffic share and marketing efficiency, and its strength in alternative accommodations. These are growing faster than hotels and reached 34% of lodging room nights during the third quarter, which was notable as Booking has yet to reach full feature parity versus rival Airbnb (ABNB) — suggesting there is some room to grow there.

Our health care holdings also fared well. The sector has been largely overlooked in 2023 amid AI exuberance, but its defensiveness is looking more salutary as tighter monetary policy begins to sap market sentiment. Novo Nordisk (NVO) shares rose on continued unprecedented demand for GLP-1s, which treat diabetes and obesity, and of which Novo Nordisk is one of two major providers. GLP-1s represent the largest commercial opportunity and investable theme in health care.

Other health care holdings such as managed care company UnitedHealth Group (UNH) and health care services company CVS Health (CVS) were also rewarded in the third quarter. UnitedHealth, which beat expectations and raised full-year guidance, demonstrated that the recent Medicare utilization uptick was manageable and relatively short term. CVS, though a marginal contributor, has been weighed down in 2023 by an acquisition deal for Oak Street Health, an increase in medical benefits costs and a decline in the company’s overall Medicare Advantage star rating, but recent operational improvements suggest progress in its transition from a retailer to a diversified health care services company. Oak Street Health is a potential foundational asset for CVS’s retail primary care strategy, and we are positive on the company’s long-term prospects.

We continue to be active in positioning our holdings in the health care sector, in the quarter initiating a new position in Hologic (HOLX), a medical technology company focused on women’s health with leading positions in medical diagnostics, medical imaging systems and surgical devices. The company has used profits generated during the pandemic to diversify the business and increase recurring revenues, as well as return capital to shareholders. We believe Hologic is well-positioned to drive stable growth and improve profitability going forward and has a very strong balance sheet to fund future growth initiatives. Hologic’s products help detect cancer as well as a variety of infectious diseases, including COVID-19, thus improving health care outcomes for patients.

Outlook

While the Federal Reserve may be nearing or at the end of its tightening cycle, we believe the lagging impacts of 525 bps of interest rate hikes in the last 18 months will be felt on corporate and consumer balance sheets well into the future. While maintaining our fundamental, bottom-up process, the portfolio’s underweights to the consumer discretionary and communication services sectors partially reflect our cognizance of this risk. We are comfortable, at the same time, with overweights to more defensive health care and consumer staples sectors, as well as to the industrials sector where secular trends such as energy efficiency and decarbonization are long-term drivers for our holdings. We continue to focus on investing in companies that we believe can outperform through full market cycles, and remain firmly convinced that high-quality companies with leading sustainability profiles will prove to be rewarding long-term investments.

Portfolio Highlights

The ClearBridge Sustainability Leaders Strategy underperformed its Russell 3000 Index benchmark during the third quarter. On an absolute basis, the Strategy had gains in two of 10 sectors in which it was invested (out of 11 sectors total). The sole contributors were the communication services and consumer discretionary sectors, while the information technology (IT) and utilities sectors were the main detractors.

On a relative basis, overall stock selection and sector allocation detracted. Stock selection in the IT, utilities and materials sectors were the main detractors. Conversely, stock selection in the health care and consumer discretionary sectors was positive. A lack of energy holdings detracted.

On an individual stock basis, Williams-Sonoma, Booking, Alphabet (GOOG)(GOOGL), Novo Nordisk and Eaton were the largest contributors to absolute performance in the quarter. The main detractors from absolute returns were positions in Apple (AAPL), SolarEdge Technologies, NextEra Energy Partners, LP, Microsoft (MSFT) and Keysight Technologies (KEYS).

Other positioning moves involved the sale of Progressive (PGR) and the addition of Travelers (TRV). Progressive has had a challenging time pricing in line with elevated loss trends, although we believe it will be able to improve its combined ratio over time. After a rebound in shares, we felt the risk reward was superior at Travelers, which is both more diversified and less expensive, in our view.

ESG Highlights

The Company’s Role as Steward of Biodiversity

The push to halt biodiversity loss is increasingly demanding attention alongside climate change as a major environmental concern for investors. As we explore elsewhere in a recent ClearBridge introduction and discussion of the topic, the term biodiversity, meaning the variety of life on the planet or in a given ecosystem, is emerging as an umbrella concept for several related environmental concerns. These include issues tied to changes in land usage (such as deforestation), natural resource overexploitation, pollution and the effects of climate change.

On the international stage, in an agreement recalling the 2015 Paris Agreement, attendees of the 2022 United Nations Biodiversity Conference adopted the Kunming-Montreal Global Biodiversity Framework (GBF), a plan for member countries to take urgent action to halt and reverse biodiversity loss and to conserve and sustainably use biodiversity.

“Improving biodiversity is already an economic concern for many companies.”

As a result, regulation is stepping up. In May, an EU regulation on deforestation-free supply chains, for example, began requiring companies to confirm imported products have not been produced on land subject to deforestation or forest degradation, with fines of at least 4% of the company’s annual income in the EU at stake.

In September, the Taskforce on Nature-Related Financial Disclosures (TNFD), which was launched in 2021, published recommendations on the types of biodiversity disclosures companies can and should be making. These generally involve companies disclosing how their businesses both impact and depend on nature, what related material risks and opportunities they are assessing, and what metrics and targets they are using to measure and improve. As the TNFD points out, “Present and future cash flows depend on the flow of nature’s inputs to business and accelerating nature loss poses a growing risk to businesses and capital providers.”

The materiality of biodiversity issues for public equities helps explain why ClearBridge has, over 35+ years of our ESG integration approach, assessed evolving nature-related dependencies, impacts, risks and opportunities with holdings across sectors. To support our fundamental research and steer capital in a nature-positive way, ClearBridge encourages, among other things, assessment and disclosure of nature-related impacts and dependencies within the value chain, development of biodiversity and deforestation policies, responsible waste and water management, transparency into lending practices, and consideration of local affected communities.

Nature-positive revenue opportunities tend to be tied to companies with products that either substitute for a high-impact product (ClearBridge holding Ball’s aluminum containers reduce the need for mining ore and extracting oil and are a substitute for single-use plastic, a major polluter) or reduce impact (ClearBridge holding Deere’s precision agriculture technologies limit pollution in the form of chemical pesticides and herbicides). Both types are found across ClearBridge portfolios, as well as companies providing key financing for nature-positive solutions.

Reducing Impact: Untroubling Waters

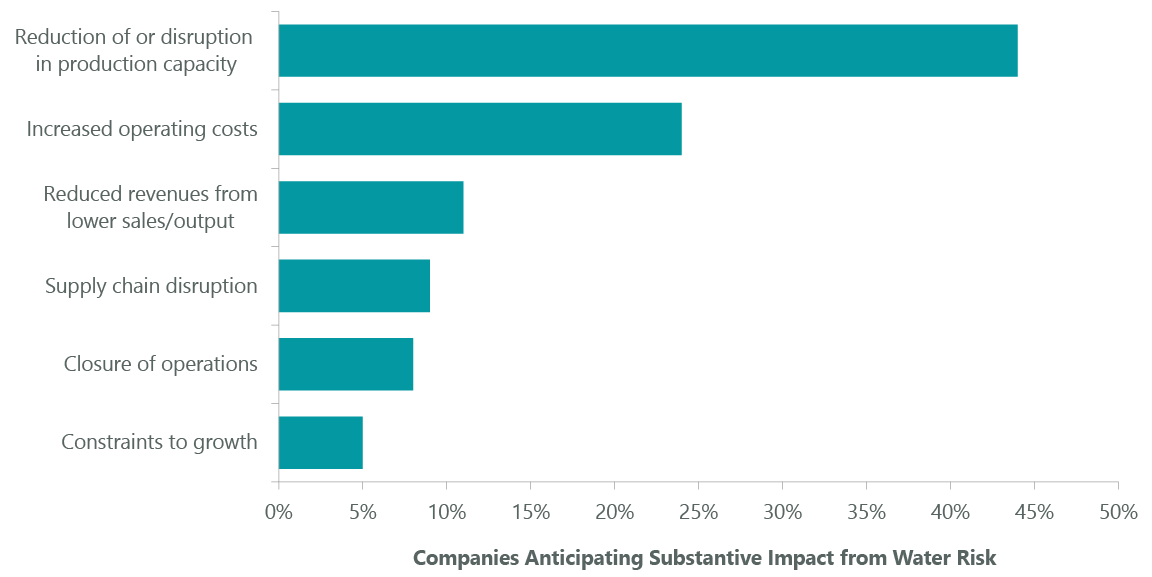

Water looms large as a high-impact natural resource, both in its use in business and its importance to virtually every ecosystem. Of companies disclosing on water via CDP, formerly the Carbon Disclosure Project, that are exposed to substantive impacts on their business from water, most anticipate that water issues could limit the growth of their business through reducing/disrupting production capacity, closure of operations or constraints to growth (Exhibit 1).

Exhibit 1: Potential Impacts of Water Risk in Direct Operations and Supply Chain

Source: High and Dry: How Water Issues Are Stranding Assets, A report commissioned by the Swiss Federal Office for the Environment (FOEN). May 2022.

Long-time ClearBridge holding Ecolab (ECL) stands out as a responsible steward of water resources and a company able to reduce impact from use of water across the economy. Ecolab offers water-saving solutions for laundries used by health care, hospitality and food and beverage industries. Products and services include industrial water pre-treatment systems, industrial water reuse, water-efficient conveyor lubrication systems and wastewater treatment. For a major hotel chain, Ecolab’s chemical product delivery service replaces single-use drums of cleaning chemical, reducing waste and improving work safety, while its warewashing and housekeeping solutions reduce wash time, water usage and water temperature for food prep wares as well as plastic packaging used in housekeeping services. Ecolab estimates 57 million gallons of water savings as well as 1,400 metric tons of GHG emissions annually for the hotel chain as a result.

Ecolab has committed to helping its customers conserve 300 billion gallons of water a year, equivalent to the annual drinking water needs of 1 billion people by 2030, through reducing water withdrawal needs in customers’ operations. Separately, Ecolab also has a target to restore >50% of its absolute water withdrawal at high-risk sites through collaboration with NGOs and local communities. Ecolab is also a co-founder of the Water Resilience Coalition, a CEO-led movement and part of the United Nations Global Compact aiming to preserve the world’s freshwater resources through action in water-stressed basins.

Reducing Impact: Sustainable Forestry

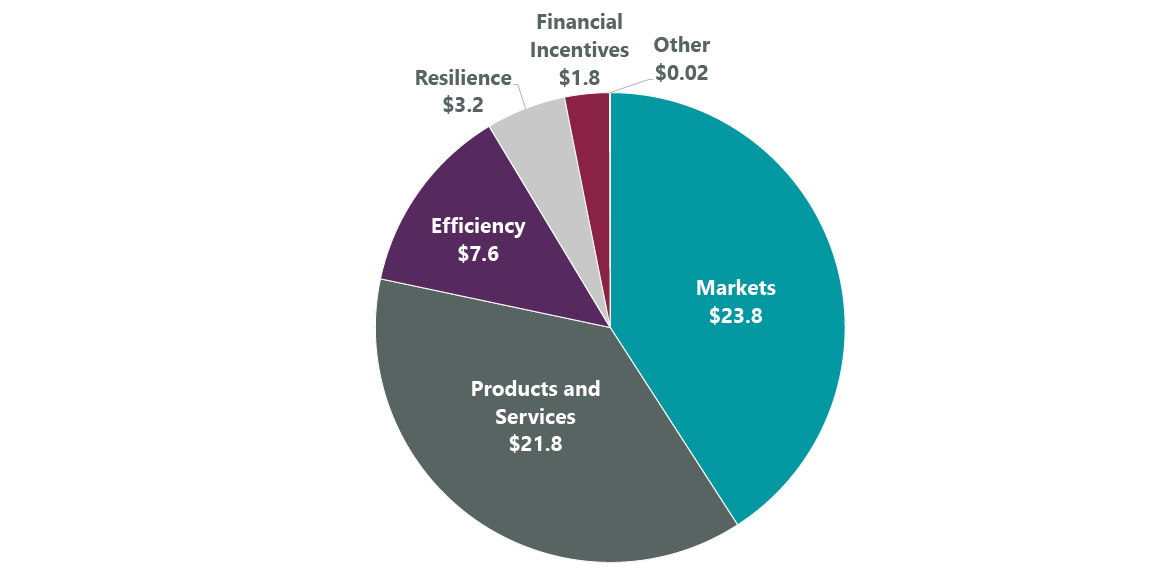

There are also benefits for companies that recognize and mitigate deforestation risks (Exhibit 2). Broadly, these may include, increased brand value, demand for certified or deforestation-free materials, availability of products with reduced environmental impact, supply chain transparency and resilience.1

Exhibit 2: Potential Financial Impact of Reported Forest-Related Opportunities (Billions)

Source: “The Forest Transition: From Risk to Resilience,” Global Forests Report 2023, CDP. July 2023. Shows forest-related opportunities identified by 231 companies reporting. Markets include increased demand for certified materials or products with reduced environmental impact; resilience includes greater supply chain resilience and climate change adaptation; products and services includes increased brand value and R&D and innovation opportunities; efficiency includes increased efficiency of manufacturing and distribution processes and cost savings; financial incentives include issuing green bonds and earning a price premium for deforestation-free materials.

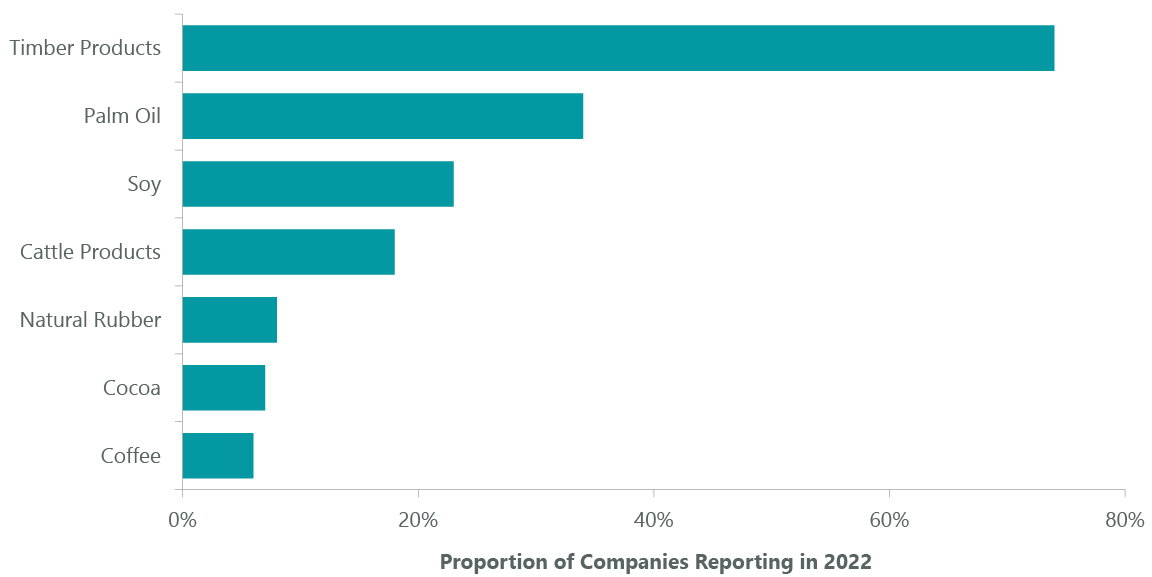

Home Depot (HD) has long been a leader in advancing sustainable forestry, and its wood products can have a significant impact, as timber rates at the top of high-risk commodities responsible for most agriculture-related deforestation (Exhibit 3). The home improvement retailer adopted its first wood purchasing policy in 1999, pledging to give preference to sustainably sourced wood and to eliminate wood purchases from endangered regions around the world.

Biodiversity-boosting efforts at Home Depot have included tracing the origin of all the wood products it sells. This forms part of the process of verifying sustainable production, which it does using the certification standards of the Forest Stewardship Council (FSC). Since 2000 Home Depot has developed programs to purchase FSC wood products, such as doors, boards and patio furniture, from over 60 global suppliers. It has also moved more than 90% of its cedar purchases to second-and third-growth forests, with the rest coming from areas with local community stakeholder review.

Exhibit 3: High-Risk Commodities for Agriculture-Related Deforestation

Source: “The Forest Transition: From Risk to Resilience,” Global Forests Report 2023, CDP. July 2023. Of 810 companies disclosing on at least one of the seven high-risk commodities, equaling 1,375 commodity-level disclosures.

Suppliers preferred by Home Depot such as Mendocino Redwood Company also help maintain sustainable forests through building forests’ wildfire resilience. For example, Mendocino practices fuel reduction by removing excess burnable materials that helps wildfires stay closer to the ground where they can be more safely controlled by firefighters before they reach the forest canopy.

Substituting Impact: Preventing Deforestation

ClearBridge holding Trex (TREX) has redefined the decking industry with a business model that addresses two key drivers of biodiversity loss, deforestation and pollution, by substituting high-impact products. Instead of relying on virgin wood, Trex makes composite decking for residential and commercial customers using 95% recycled wood fibers and plastic waste. In 2022, Trex recycled 337 million pounds of waste polyethylene, a plastic commonly used for plastic bags and bottles, as it produced its high-end decking. Wood decks stopped using arsenic treatments in 2004, which has shortened their life span, dramatically increasing the number of decks that need to be replaced. Trex’s products help fill this need in a way that preserves forests, reduces a major source of pollution in oceans, and lowers customers’ total costs of ownership, since Trex’s decks have much longer lifespans relative to natural lumber decks.

Financing Biodiversity

In addition to business models that support biodiversity, it is also important to provide financing for efforts to improve biodiversity. Large financial firms such as ClearBridge holding JPMorgan Chase (JPM) have a key role here through green bond underwritings that support natural capital protection. In 2021 JPM announced a target to finance and facilitate $1 trillion toward green initiatives by 2030 as part of its broader $2.5 billion sustainable development target. The green initiatives include biodiversity-linked areas such as water management, circular economy and waste management, in addition to conservation and biodiversity, which focuses on improving terrestrial and aquatic biodiversity ecosystems or forests.

As part of this target, in 2022 JPM served as the lead underwriter for a $350 million green bond issued by The Nature Conservancy, the largest green bond issuance by a conservation nonprofit ever. The issuance is expected to help The Nature Conservancy avoid or sequester 3 billion metric tons of carbon dioxide equivalent (CO2e), and conserve 650 million hectares of healthy land, 30 million hectares of freshwater and 4 billion hectares of oceans.

Nature-Based Carbon Credits: Early Stages

JPM also highlights the value of nature-based carbon credits: these are credits a company can purchase to fund nature-based solutions to climate change to help offset its own emissions. For JPM, in addition to sourcing renewable energy to reduce its carbon footprint, it also purchases high-quality nature-based carbon credits that help restore the natural world, helping to offset the remainder of its emissions. One purchase in 2022 was from the Indus Delta Blue Carbon Project in southeastern Pakistan, one of the largest mangrove forest restoration projects in the world. Mangroves are among the world’s most diverse and vulnerable ecosystems and are effective carbon sinks; in this case they are also important habitats for endangered and threatened species and serve as a protective barrier, mitigating potential damage from hurricanes and tsunamis.

Conclusion

Improving biodiversity is already an economic concern for many companies. While developing standardized measurements of biodiversity remains an industry challenge, international agreements are spurring policy action, and the materiality of biodiversity for companies is poised to increase. As it does, ClearBridge will continue to analyze and engage companies on nature-related risks and opportunities, seeking to build more resilient businesses in a more resilient world.

By Derek Deutsch, CFA, Managing Director, Portfolio Manager

Mary Jane McQuillen, Head of ESG, Portfolio Manager

Past performance is no guarantee of future results. Copyright © 2023 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information.

Performance source: Internal. Benchmark source: Russell Investments. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication.

1 “The Forest Transition: From Risk to Resilience,” Global Forests Report 2023, CDP. July 2023. Page 36.

Original Post

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here