DKosig

By Peter Bourbeau & Margaret Vitrano

Engaging Large Caps on Nature-Related Risks

Market Overview

Equities took a breather in the third quarter, pressured by rising bond yields, a hawkish turn by the Federal Reserve and signs of late cycle spending fatigue. The S&P 500 Index (SP500, SPX) fell 3.27% while the Nasdaq Composite declined 4.10% as the Fed indicated that generationally high interest rates could remain elevated well into 2024. The benchmark Russell 1000 Growth Index gave back some gains, dropping 3.13% and performing mostly in line with the Russell 1000 Value Index (-3.17%). Growth remains ahead of value by over 2,300 basis points year-to-date.

The 10-year Treasury yield climbed 74 bps during the quarter, reaching its highest level in 16 years (Exhibit 1). Surging yields have resulted from resilient economic data and a rebound in inflation that caused the Fed to push out any hopes of a rate cut in the near future. While the central bank may be nearing or at the end of its tightening cycle, we believe the lagging impacts of 525 bps of interest rate hikes in the last 18 months will be felt on corporate and consumer balance sheets well into the future.

Energy (+15.26%) and communication services (+5.19%) were the only sectors in the benchmark to deliver gains for the quarter while health care (-0.10%) and financials (-0.54%) also outperformed. Utilities (-12.61%), real estate (-11.29%) and consumer staples (-6.72%) were the worst performers, followed by materials (-5.96%) and information technology (IT, -5.92%) while consumer discretionary (-3.18%) finished mostly in line with the benchmark.

Exhibit 1: Rising Yields Again Pressuring Growth Stocks

| *Growth Outperformance indicates quarterly periods where the Russell 1000 Growth Index outperformed the Russell 1000 Value Index. Data as of Sept. 30, 2023. Source: FactSet. |

The ClearBridge Large Cap Growth ESG Strategy underperformed for the quarter, as weakness in our higher multiple medical device holdings and consumer names with direct exposure to China weighed on performance. Year-to-date relative performance remains solid, supported by positive stock selection that has more than offset being underweight strongly performing mega caps Apple (AAPL) and Microsoft (MSFT). The quarterly underperformance of those two stocks, the largest in the benchmark, added to relative performance. Such results suggest that our focus on diversification should keep the Strategy well-positioned in a market we expect to remain unsettled.

Positive clinical trials showing cardiovascular benefits for GLP-1 diabetes and obesity therapeutic semaglutide boosted shares of portfolio holding Eli Lilly (LLY), which markets Mounjaro for these conditions. However, the potential for improved patient outcomes raised the risk of lower utilization for DexCom (DXCM), a maker of continuous glucose monitoring devices, and Intuitive Surgical (ISRG), whose robotic surgical systems are used in weight loss procedures. While headline risk to these stocks is unlikely to go away soon, we believe any financial impact from GLP-1s will be restrained due to a limited current patient population and the need to continue to treat progressive diseases, like diabetes, through regular monitoring.

Athletic footwear and apparel marketer Nike (NKE) and cosmetics maker Estee Lauder (EL) also lagged during the quarter due to consumer weakness in China, a core market for both companies. The world’s second largest economy continues to be held back by a tepid COVID-19 recovery and weakness in its sprawling property sector. As the marginal consumer of everything from commodities to smartphones, we are closely monitoring Chinese demand and our exposures there.

Offsetting these areas of softness, we were pleased with the positive contributions from our IT holdings. Data monitoring software maker Splunk (SPLK) re-rated on a takeout offer from Cisco Systems (CSCO), while workflow software maker Atlassian (TEAM) and newer position Intuit (INTU) delivered solid results. Shares of Nvidia (NVDA) , the clear leader in supplying graphics processing units to power AI applications, finished the quarter on an upswing and remain substantially higher for the year. Nvidia’s multiple has actually compressed year-to-date due to better-than-expected earnings growth and, while we remain confident in the company’s long-term growth trajectory, we trimmed the position for the third time this year to manage our overall portfolio risk.

Portfolio Positioning

We maintained our “moving to the middle” approach to positioning in the third quarter, taking profits in medical devices and animal health to trim our health care overweight and provide funds for repositioning into areas earlier in their growth cycle.

Investing in growth companies going through earnings resets has proved effective during the recent period of improved Strategy performance. Long time holding Amazon.com (AMZN) and new addition Target (TGT) are the latest examples of businesses that have likely seen their profit forecasts bottom. We added to Amazon during the quarter, as the company has demonstrated progress in improving retail profitability after a large period of investment during COVID-19 and because its AWS cloud business has shown signs of growth stabilization.

Big box retailer Target provides early-cycle consumer exposure, but with support from cash flow and a dividend. Target reset earnings in August by lowering its full-year outlook to account for weak sales and one-time cost issues, leaving its shares trading at a historically wide discount to peers Wal-Mart and Costco. We see the company as a turnaround story, with better-than-expected margin and inventory controls leading to improved comparisons. In addition, we view the controversy around Target’s Pride merchandise assortment, and consequent backlash, to be fixable. A deeper-than-expected downturn in consumer spending and a failure to reverse traffic declines and recent market share losses are risks to our thesis, but we believe they are sufficiently accounted for in the stock’s current valuation.

New addition Union Pacific (UNP) also falls in our cyclical bucket of companies working through short-term headwinds. The rail operator provides the added benefit of a low correlation to the rest of the portfolio. As an efficient way to transport grain, coal and autos and with networks that extend from Mexico through the U.S. to Canada, the freight rail industry generates high returns on invested capital and is positioned to benefit from reshoring. We have been researching rails for the last 18 months, waiting for earnings estimates to come down amidst a weakening macro backdrop. By the start of the third quarter we believe estimates had declined enough to make us comfortable in establishing exposure. We chose Union Pacific as its risk-reward is compelling if the turnaround being led by new CEO Jim Vena is successful. Rail volumes are coincident with macro conditions, causing us to establish a minimal position that can be built opportunistically.

We exited Sea Limited (SE), which has experienced headwinds in its gaming and e-commerce businesses since COVID-19 began to recede. Sea began rapidly moving toward profitability in 2022 and we expected management to continue down that path. However, the company announced a pivot back to re-investing for growth in e-commerce early in the quarter which we believe makes for too many strategic pivots in a short time, causing diminished shareholder confidence and delays in the stock’s value realization. This, combined with tightening up the portfolio’s exposure to international and economically sensitive end markets, ultimately led to the sale.

Outlook

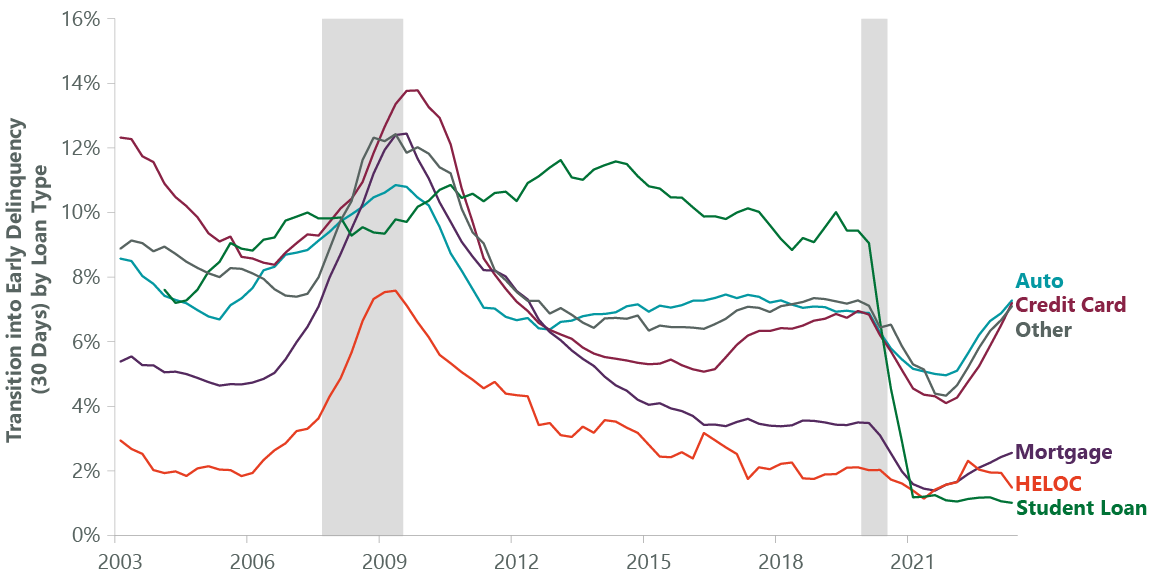

The U.S. economy remains on the precipice of a recession or soft landing, with inflation and labor costs moderating. We are very late in the current cycle and expect stocks will bottom ahead of company fundamentals. We are already seeing this in areas like consumer discretionary as earnings have weakened, consumer credit balances are increasing and credit quality is worsening (Exhibit 2). The industrial complex is starting to normalize as pandemic supply dislocations and the benefits of inflation are going away. On the enterprise level, businesses are becoming more austere and managing budgets more tightly.

These worsening conditions support the goals of recent portfolio activity. A soft landing could lead to a period of low GDP growth like 2014-2016, where a company’s ability to generate organic growth and self-fund future investments were important. We believe the portfolio is well-exposed to these types of fundamentally sound growth franchises.

Our holdings in the stable growth bucket, like Visa and UnitedHealth Group, have done a good job managing earnings in more volatile periods, and should be able to execute well through the economy’s normalizing process. We also have cyclical companies delivering strong operating earnings growth like Grainger, Eaton and Uber.

Exhibit 2: Rising Delinquency Rates Could Slow Spending

| HELOC stands for Home Equity Line of Credit. Data as of June 30, 2023, latest available as of Sept. 30, 2023. Source: NY Fed, Equifax. |

Finally, we are confident in our select growth exposure. These companies are being driven by earnings growth rather than multiple expansion, and maintain reasonable valuations compared to other parts of the IT and communication services sectors. The Strategy remains overweight enterprise software, where holdings like Adobe and Salesforce are seeing business trends stabilize. Online advertising is also seeing a healthy recovery which should benefit META Platforms and Amazon.

In addition to stable grower Microsoft, many of our select names are directly indexed to the secular growth of artificial intelligence (AI). Our research efforts, supported by ClearBridge’s sector analysts, are focused on new use cases as inference models ramp up, as well as determining which software and services companies will be supplanted by AI and which will remain relevant. Success will likely be a function of who has the best proprietary data to offer enhanced services, a setup where we see large companies as having an advantage over startups.

Portfolio Highlights

The ClearBridge Large Cap Growth ESG Strategy underperformed its benchmark in the third quarter. On an absolute basis, the Strategy posted losses across the 10 sectors in which it was invested (out of 11 sectors total). The primary detractors from performance were the IT and health care sectors.

Relative to the benchmark, overall stock selection detracted from performance. In particular, stock selection in the communication services, health care, financials and consumer staples sectors and an underweight to communication services weighed on results. On the positive side, stock selection and an underweight allocation to the IT sector contributed the most to performance.

On an individual stock basis, the leading absolute contributors were positions in Splunk, Nvidia, Atlassian, Meta Platforms and UnitedHealth Group (UNH). The primary detractors were Microsoft, Apple, Netflix (NFLX), DexCom and Estee Lauder.

ESG Highlights

The Company’s Role as a Steward of Biodiversity

The push to halt biodiversity loss is increasingly demanding attention alongside climate change as a major environmental concern for investors. As we explore elsewhere in a recent ClearBridge introduction and discussion of the topic, the term biodiversity, meaning the variety of life on the planet or in a given ecosystem, is emerging as an umbrella concept for several related environmental concerns. These include issues tied to changes in land usage (such as deforestation), natural resource overexploitation, pollution and the effects of climate change.

On the international stage, in an agreement recalling the 2015 Paris Agreement, attendees of the 2022 United Nations Biodiversity Conference adopted the Kunming-Montreal Global Biodiversity Framework (GBF), a plan for member countries to take urgent action to halt and reverse biodiversity loss and to conserve and sustainably use biodiversity.

As a result, regulation is stepping up. In May, an EU regulation on deforestation-free supply chains, for example, began requiring companies to confirm imported products have not been produced on land subject to deforestation or forest degradation, with fines of at least 4% of the company’s annual income in the EU at stake.

In September, the Taskforce on Nature-Related Financial Disclosures (TNFD), which was launched in 2021, published recommendations on the types of biodiversity disclosures companies can and should be making. These generally involve companies disclosing how their businesses both impact and depend on nature, what related material risks and opportunities they are assessing, and what metrics and targets they are using to measure and improve. As the TNFD points out, “Present and future cash flows depend on the flow of nature’s inputs to business and accelerating nature loss poses a growing risk to businesses and capital providers.”

The materiality of biodiversity issues for public equities helps explain why ClearBridge has, over 35+ years of our ESG integration approach, assessed evolving nature-related dependencies, impacts, risks and opportunities with holdings across sectors. To support our fundamental research and steer capital in a nature-positive way, ClearBridge encourages, among other things, assessment and disclosure of nature-related impacts and dependencies within the value chain, development of biodiversity and deforestation policies, responsible waste and water management, transparency into lending practices, and consideration of local affected communities.

Nature-positive revenue opportunities tend to be tied to companies with products that either substitute for a high-impact product (ClearBridge holding Ball’s aluminum containers reduce the need for mining ore and extracting oil and are a substitute for single-use plastic, a major polluter) or reduce impact (ClearBridge holding Deere’s precision agriculture technologies limit pollution in the form of chemical pesticides and herbicides). Both types are found across ClearBridge portfolios, as well as companies providing key financing for nature-positive solutions.

Reducing Impact: Untroubling Waters

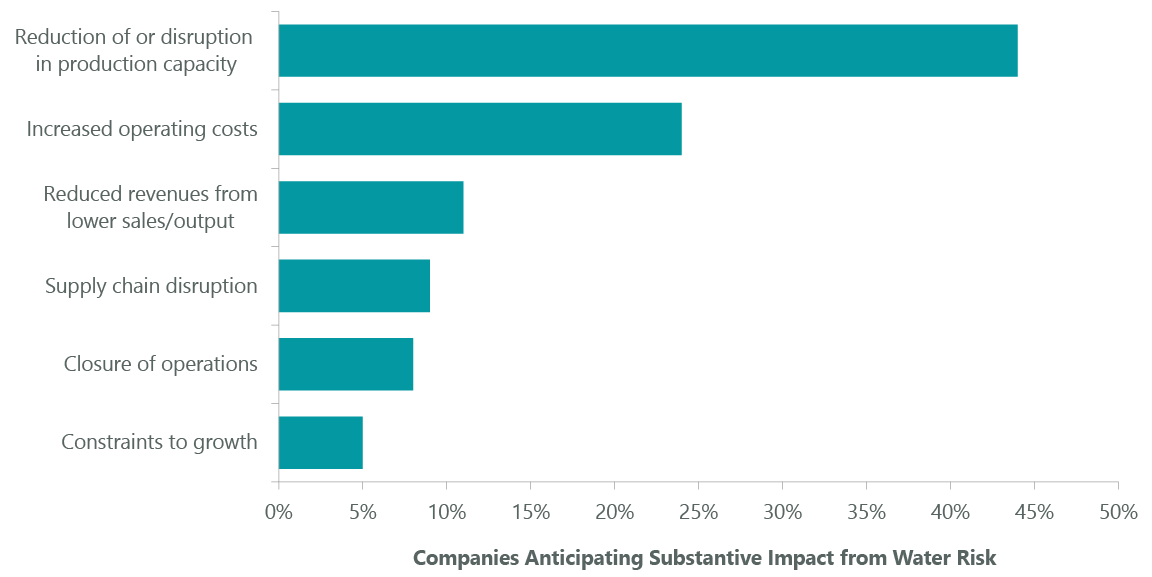

Water looms large as a high-impact natural resource, both in its use in business and its importance to virtually every ecosystem. Of companies disclosing on water via CDP, formerly the Carbon Disclosure Project, that are exposed to substantive impacts on their business from water, most anticipate that water issues could limit the growth of their business through reducing/disrupting production capacity, closure of operations or constraints to growth (Exhibit 3).

Exhibit 3: Potential Impacts of Water Risk in Direct Operations and Supply Chain

| Source: High and Dry: How Water Issues Are Stranding Assets, A report commissioned by the Swiss Federal Office for the Environment (FOEN). May 2022. |

Long-time ClearBridge holding Ecolab (ECL) stands out as a responsible steward of water resources and a company able to reduce impact from use of water across the economy. Ecolab offers water-saving solutions for laundries used by health care, hospitality and food and beverage industries. Products and services include industrial water pre-treatment systems, industrial water reuse, water-efficient conveyor lubrication systems and wastewater treatment. For a major hotel chain, Ecolab’s chemical product delivery service replaces single-use drums of cleaning chemical, reducing waste and improving work safety, while its warewashing and housekeeping solutions reduce wash time, water usage and water temperature for food prep wares as well as plastic packaging used in housekeeping services. Ecolab estimates 57 million gallons of water savings as well as 1,400 metric tons of GHG emissions annually for the hotel chain as a result.

Ecolab has committed to helping its customers conserve 300 billion gallons of water a year, equivalent to the annual drinking water needs of 1 billion people by 2030, through reducing water withdrawal needs in customers’ operations. Separately, Ecolab also has a target to restore >50% of its absolute water withdrawal at high-risk sites through collaboration with NGOs and local communities. Ecolab is also a co-founder of the Water Resilience Coalition, a CEO-led movement and part of the United Nations Global Compact aiming to preserve the world’s freshwater resources through action in water-stressed basins.

Reducing Impact: Sustainable Forestry

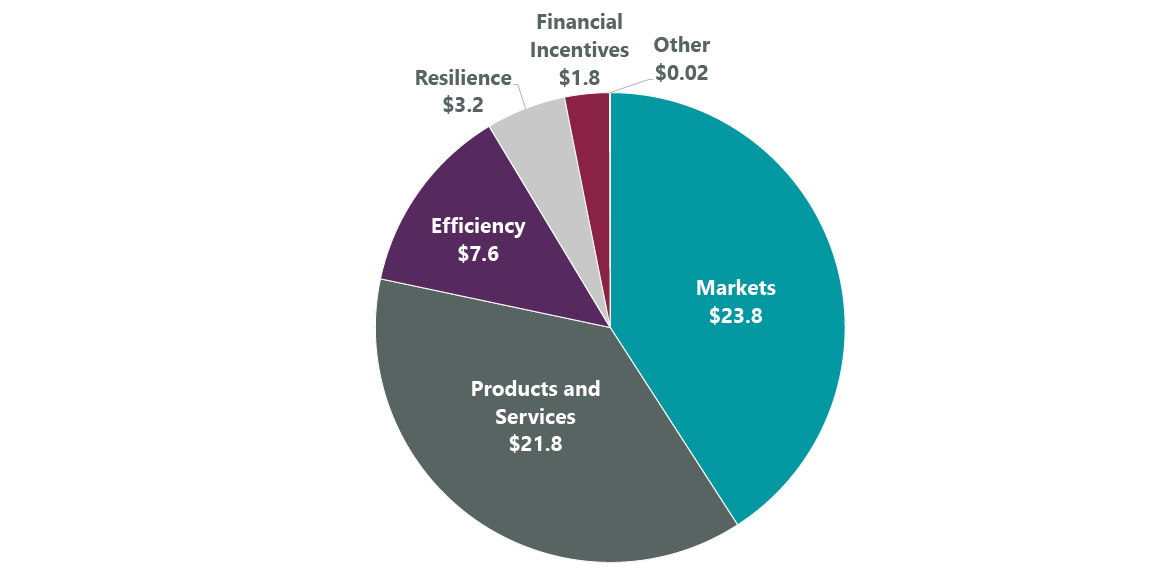

There are also benefits for companies that recognize and mitigate deforestation risks (Exhibit 4). Broadly, these may include, increased brand value, demand for certified or deforestation-free materials, availability of products with reduced environmental impact, supply chain transparency and resilience.1

Exhibit 4: Potential Financial Impact of Reported Forest-Related Opportunities (Billions)

| Source: “The Forest Transition: From Risk to Resilience,” Global Forests Report 2023, CDP. July 2023. Shows forest-related opportunities identified by 231 companies reporting. Markets include increased demand for certified materials or products with reduced environmental impact; resilience includes greater supply chain resilience and climate change adaptation; products and services includes increased brand value and R&D and innovation opportunities; efficiency includes increased efficiency of manufacturing and distribution processes and cost savings; financial incentives include issuing green bonds and earning a price premium for deforestation-free materials. |

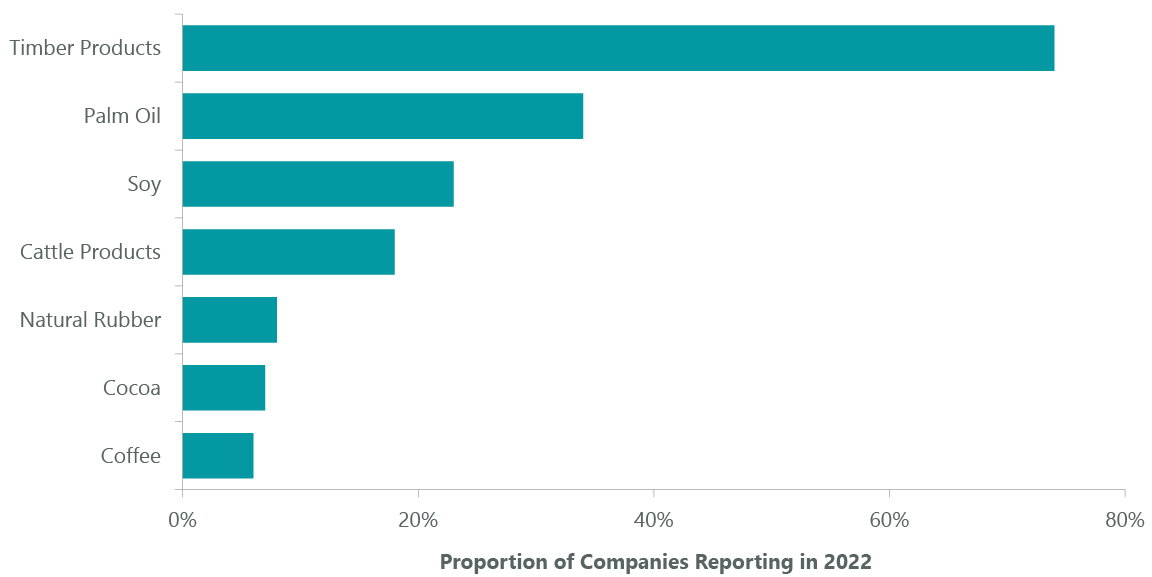

Home Depot (HD) has long been a leader in advancing sustainable forestry, and its wood products can have a significant impact, as timber rates at the top of high-risk commodities responsible for most agriculture-related deforestation (Exhibit 5). The home improvement retailer adopted its first wood purchasing policy in 1999, pledging to give preference to sustainably sourced wood and to eliminate wood purchases from endangered regions around the world.

Biodiversity-boosting efforts at Home Depot have included tracing the origin of all the wood products it sells. This forms part of the process of verifying sustainable production, which it does using the certification standards of the Forest Stewardship Council (FSC). Since 2000 Home Depot has developed programs to purchase FSC wood products, such as doors, boards and patio furniture, from over 60 global suppliers. It has also moved more than 90% of its cedar purchases to second-and third-growth forests, with the rest coming from areas with local community stakeholder review.

Exhibit 5: High-Risk Commodities for Agriculture-Related Deforestation

| Source: “The Forest Transition: From Risk to Resilience,” Global Forests Report 2023, CDP. July 2023. Of 810 companies disclosing on at least one of the seven high-risk commodities, equaling 1,375 commodity-level disclosures. |

Suppliers preferred by Home Depot such as Mendocino Redwood Company also help maintain sustainable forests through building forests’ wildfire resilience. For example, Mendocino practices fuel reduction by removing excess burnable materials that helps wildfires stay closer to the ground where they can be more safely controlled by firefighters before they reach the forest canopy.

Substituting Impact: Preventing Deforestation

ClearBridge holding Trex has redefined the decking industry with a business model that addresses two key drivers of biodiversity loss, deforestation and pollution, by substituting high-impact products. Instead of relying on virgin wood, Trex makes composite decking for residential and commercial customers using 95% recycled wood fibers and plastic waste. In 2022, Trex recycled 337 million pounds of waste polyethylene, a plastic commonly used for plastic bags and bottles, as it produced its high-end decking. Wood decks stopped using arsenic treatments in 2004, which has shortened their life span, dramatically increasing the number of decks that need to be replaced. Trex’s products help fill this need in a way that preserves forests, reduces a major source of pollution in oceans, and lowers customers’ total costs of ownership, since Trex’s decks have much longer lifespans relative to natural lumber decks.

Financing Biodiversity

In addition to business models that support biodiversity, it is also important to provide financing for efforts to improve biodiversity. Large financial firms such as ClearBridge holding JPMorgan Chase (JPM) have a key role here through green bond underwritings that support natural capital protection. In 2021 JPM announced a target to finance and facilitate $1 trillion toward green initiatives by 2030 as part of its broader $2.5 billion sustainable development target. The green initiatives include biodiversity-linked areas such as water management, circular economy and waste management, in addition to conservation and biodiversity, which focuses on improving terrestrial and aquatic biodiversity ecosystems or forests.

As part of this target, in 2022 JPM served as the lead underwriter for a $350 million green bond issued by The Nature Conservancy, the largest green bond issuance by a conservation nonprofit ever. The issuance is expected to help The Nature Conservancy avoid or sequester 3 billion metric tons of carbon dioxide equivalent (CO2e), and conserve 650 million hectares of healthy land, 30 million hectares of freshwater and 4 billion hectares of oceans.

Nature-Based Carbon Credits: Early Stages

JPM also highlights the value of nature-based carbon credits: these are credits a company can purchase to fund nature-based solutions to climate change to help offset its own emissions. For JPM, in addition to sourcing renewable energy to reduce its carbon footprint, it also purchases high-quality nature-based carbon credits that help restore the natural world, helping to offset the remainder of its emissions. One purchase in 2022 was from the Indus Delta Blue Carbon Project in southeastern Pakistan, one of the largest mangrove forest restoration projects in the world. Mangroves are among the world’s most diverse and vulnerable ecosystems and are effective carbon sinks; in this case they are also important habitats for endangered and threatened species and serve as a protective barrier, mitigating potential damage from hurricanes and tsunamis.

Conclusion

Improving biodiversity is already an economic concern for many companies. While developing standardized measurements of biodiversity remains an industry challenge, international agreements are spurring policy action, and the materiality of biodiversity for companies is poised to increase. As it does, ClearBridge will continue to analyze and engage companies on nature-related risks and opportunities, seeking to build more resilient businesses in a more resilient world.

Peter Bourbeau, Managing Director, Portfolio Manager

Margaret Vitrano, Managing Director, Portfolio Manager

|

Past performance is no guarantee of future results. Copyright © 2023 ClearBridge Investments. All opinions and data included in this commentary are as of the publication date and are subject to change. The opinions and views expressed herein are of the author and may differ from other portfolio managers or the firm as a whole, and are not intended to be a forecast of future events, a guarantee of future results or investment advice. This information should not be used as the sole basis to make any investment decision. The statistics have been obtained from sources believed to be reliable, but the accuracy and completeness of this information cannot be guaranteed. Neither ClearBridge Investments, LLC nor its information providers are responsible for any damages or losses arising from any use of this information. Performance source: Internal. Benchmark source: Russell Investments. Frank Russell Company (“Russell”) is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company. Neither Russell nor its licensors accept any liability for any errors or omissions in the Russell Indexes and/or Russell ratings or underlying data and no party may rely on any Russell Indexes and/or Russell ratings and/or underlying data contained in this communication. No further distribution of Russell Data is permitted without Russell’s express written consent. Russell does not promote, sponsor or endorse the content of this communication. Performance source: Internal. Benchmark source: Standard & Poor’s. 1 “The Forest Transition: From Risk to Resilience,” Global Forests Report 2023, CDP. July 2023. Page 36. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here