One of the first few decisions that we may contemplate when we decide to get married is the type of matrimonial house to purchase. For the majority of us, the most practical choice would be Built-to-Order (BTO) flats. These flats are priced by HDB below market value, enabling all flat buyers to enjoy significant subsidies, excluding any housing grants.

However, if we’re someone who’s in our mid-30s or older, the completion of a BTO flat, which has a median waiting time of between 3 and 4 years, might be too long of a wait. Similarly, renting houses (no, we are not referring to the black and white bungalows) may not be ideal given the high rental market. Though there are arguments for and against renting, the general consensus is that we are better off owning our property than renting one for the long-term.

This leaves us to consider resale HDB flats as the best alternative to getting something for our immediate occupation. Among the various factors, the age of the flat is one of the considerations that flat buyers may have when purchasing a resale HDB flat. While many may argue in favour of a longer lease balance, we present four reasons why a flat with a shorter lease balance may still make good financial sense.

What Is Considered An Older Resale Flat With A Shorter Lease Balance

Before we go any further, let’s clarify what we mean by an older flat with a shorter lease balance.

Typically, HDB flats are sold on a 99-year lease, which begins the day the first homeowner takes possession of the keys to the flat from HDB. The flat owner must physically occupy the flat for a minimum occupation period (MOP) of five years before the flat can be put up for sale on the resale market.

For this article, we refer to older flats as those that have been occupied for at least 40 years or more with a remaining lease balance of 59 years or less.

Read Also: Why HDB Resale Flats Can Be Affordable If We Choose To Purchase Within Our Means

#1 The Shorter Lease Balance Flats Generally Have A Lower Price Quantum

In general, the price of a leasehold flat tends to decrease in value as the remaining lease duration becomes shorter compared to a similar flat with a longer lease balance. This is also known as lease decay. As HDB flats are primarily sold on a 99-year lease, the property/land value will fall to zero, and ownership of the land will be returned to the state upon its lease expiration.

In the tables below, we examine a small sample size of transactions based on the past six months in the towns of Ang Mo Kio and Geylang across the 3-room, 4-room, and 5-room flat types. The price difference indicates the impact of the lease balance on their respective values.

| Table 1: Ang Mo Kio | |||

| Flat Type | Location | Transaction Price | MOP (Lease Balance) |

| 3-Room | 202 – 218 Ang Mo Kio Ave 3 | $338,000 -$360,000 | 1976 (52 Years) |

| 170 – 172 Ang Mo Kio Ave 4 | $330,000 -$353,000 | 1986 (62 Years) | |

| 455A – 455C Ang Mo Kio Street 44 | $545,000 -$630,000 | 2018 (94 Years) | |

| 4-Room | 322 – 326 Ang Mo Kio Ave 3 | $510,000 -$610,000 | 1977 (53 Years) |

| 617 – 619 Ang Mo Kio Ave 4 | $545,000 -$570,000 | 1996 (72 Years) | |

| 260A – 260B Ang Mo Kio Street 21 | $825,000 -$880,000 | 2018 (95 Years) | |

| 5-Room | 401 – 437 Ang Mo Kio Ave 10 | $585,000 -$748,000 | 1979 (55 Years) |

| 253 Ang Mo Kio Street 21 | $768,000 -$838,000 | 1996 (72 Years) | |

| 455A – 455B Ang Mo Kio Street 44 | $898,000 -$1,050,000 | 2018 (95 Years) | |

| Table 2: Geylang | |||

| Flat Type | Location | Transaction Price | MOP (Lease Balance) |

| 3-Room | 19 – 24 Balam Road | $295,000 – $312,000 | 1967 (43 Years) |

| 124 – 128 Geylang East Ave 1 | $425,000 – $435,000 | 1983 (59 Years) | |

| 18A – 18D Circuit Road | $575,000 – $650,000 | 2016 (92 Years) | |

| 4-Room | 44 Sims Drive | $425,000 – $485,000 | 1975 (51 Years) |

| 28 – 30 Cassia Crescent | $755,000 – $950,000 | 1998 (74 Years) | |

| 17A – 18D Circuit Road | $770,000 – $868,000 | 2016 (92 Years) | |

| 5-Room | 13 – 23 Eunos Crescent | $597,000 – $640,000 | 1977 (53 Years) |

| 125 – 128 Geylang East Ave 1 | $765,000 – $835,000 | 1983 (59 Years) | |

| 5 – 7 Pine Close | $930,000 – $1,060,000 | 2000 (76 Years) | |

Based on a rough estimation, flat prices across the different flat types that have around 50 years or less of lease balance have transacted at around half the price of flats with over 90 years of lease balance left.

For couples who have to forgo the BTO route and are price sensitive, the shorter lease balance flats, particularly those with 50 years or less, provide a more affordable alternative.

#2 Save More On Financing Cost With Shorter Lease Balance Flats

As most of us buying a HDB flat may require some form of financing, a lower price quantum may mean not only little to no financing might be required, but we could also save more on the interest payments.

For example, let’s assume we are able to purchase a shorter-lease balance flat at $400,000 and a longer-lease balance flat at $800,000 and take 80% financing over 20 years based on the HDB concessionary loan of 2.60% per annum (p.a.). The following would be our financing costs incurred for the respective purchases:

| Shorter-Lease Balance Flat | Longer-Lease Balance Flat | |

| Loan Amount | $320,000 | $640,000 |

| Interest Rate | 2.60% | 2.60% |

| Monthly Instalment Payment | $90,717 | $181,434 |

| Total Interests | $410,717 | $821,434 |

| Total Payment | $1,711 | $3,423 |

We can see that compared to the longer-lease balance flat, we would not only pay half of the monthly instalment for the shorter-lease balance flat, but our total interest payments would also be half of the longer-lease balance flat.

This could be useful if we are starting our family lives or reaching retirement age, as it could allow us to have more cash and CPF savings, which we could then use for our immediate needs or for our retirement. Moreover, we would be less likely to tie up a large portion of our savings to our property, which is particularly important if we intend to live out the rest of our lives in the same flat, so that we can avoid the asset-rich, cash-poor syndrome.

#3 As An Investment, Shorter Lease Flats Could Give Higher Rental Yields

HDB flats, as a whole, stand out for offering one of the highest rental yields among the different residential property types. This can be attributed primarily to their lower price quantum, which is a key factor influencing rental yield. The rental yield is calculated by dividing the annual rental income by the property purchase price.

From a tenant’s perspective, the lease balance of the flat is irrelevant. Instead, they would be more concerned about other factors, such as the living condition of the flat and the location of the property. As a result, the potential income remains relatively similar across the different flat types, regardless of their lease balance.

Using the previous information in Table 2, we compare the rental income for the 3-room flat types in Geylang across the different lease balances.

| Table 3: Geylang (3-Room) | ||||

| Location | MOP (Lease Balance) | Average Price | Average Rental Income (per month) | Average Yield (per year) |

| 19 – 24 Balam Road | 1967 (43 Years) | $304,000 | $2,600 | 10% |

| 124 – 128 Geylang East Ave 1 | 1983 (59 Years) | $430,000 | $2,150 | 6% |

| 18A – 18D Circuit Road | 2016 (92 Years) | $613,000 | $2,400 | 4.70% |

As can be observed in the table above, the rental for a 3-room flat in Geylang goes for between $2,150 and $2,600. As a result of the lower price quantum, the yield on the shortest lease balance flat (19–24 Balam Road) offers an attractive yield of 10%, while the longer lease balance flats, due to their higher purchase price, have a lower yield of between 4.70% and 6%.

This strengthens the case for purchasing a shorter lease flat from an investment perspective if it is intended to be eventually rented out for income.

Read Also: Buying The Biggest HDB Flat As Your First Home: 5 Reasons Why It May Not Always Make Sense

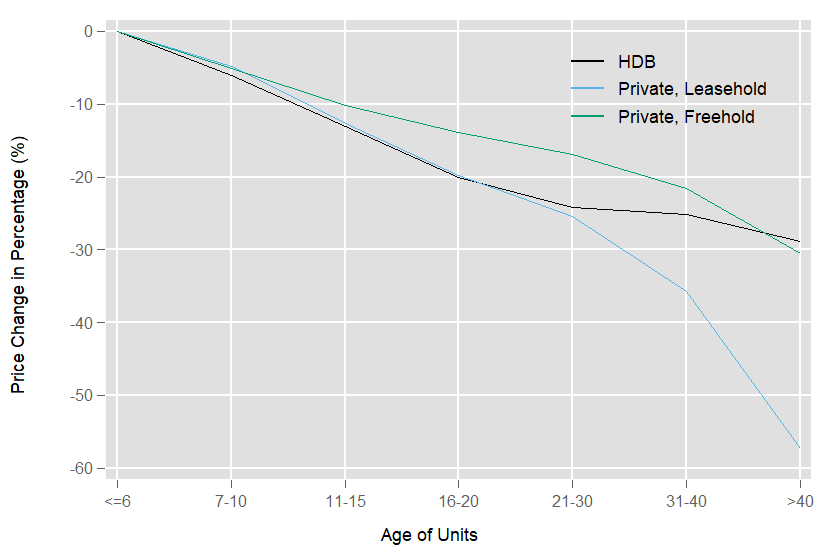

#4 Slower Rate Of Depreciation For HDB Aged 30 Years And Older

One of the concerns about buying older HDB flats is the rate of depreciation in value due to lease decay.

A study by the National University of Singapore (NUS), which looked at the depreciation rates of over 618,000 resale homes in Singapore from 1997 to 2017, discovered that:

- Depreciation rates for HDB, private leasehold, and private freehold were very similar in the first 10 years, with HDB flats depreciating only 1% faster than the other two classes of private residential properties.

- The depreciation rates of private leasehold residential properties and HDB flats are similar for up to 20 years. Thereafter, HDB flats depreciate much slower than the two classes of private residential properties.

- When properties are 21 years and older, the depreciation rate for HDB flats is only around 3%, while freehold private residential property prices depreciate by more than 10%, and leasehold private residential property prices depreciate by more than 30%.

Source: NUS

Source: NUS

The research concludes by observing that after 30 years, HDB flats have a flatter depreciation line, demonstrating that ageing slows down the resale price decline for HDB flats. This shows that, from a depreciation point of view, older flats might be generally less volatile than their mid-age HDB flat counterparts.

Read Also: Which Is The Best Value For Money Resale HDB Flat Type In Each Estate?

Should Everyone Buy Older HDB Flats With A Shorter Lease?

Buying an older HDB flat with a shorter lease balance may not be beneficial for all flat buyers, particularly for young flat buyers or those who are willing to wait for a BTO flat. After all, a BTO flat still offers us the best potential for maximising our investment return.

However, for those of us in our mid-30s or older, whether we are about to start a family life or for the more senior of us looking to downsize as we approach retirement, an older resale flat with a shorter lease could be a viable option for providing a roof over our heads.

At a later age in our lives, we may have established our roots in a particular town and not intend to move or upgrade in the future. As such, if we were to make a large property purchase, which is typically demanded of flats with longer lease balances, it could be akin to putting all our eggs in one basket. Eventually, we may not have sufficient savings and might be forced to sell and unwillingly move to another (smaller) property in our later years.

That said, if we were to consider a shorter lease balance flat, we should also be prepared that we may not see any capital gains should we sell it anytime before its lease expiration. With a shorter lease balance, the loan restriction affects the amount potential buyers can finance, which translates to a lower purchase price.

Nevertheless, it’s not all doom and gloom for flats with a shorter lease balance. The government has announced plans to provide a second round of upgrades for ageing flats at their 60- to 70-year mark as part of the Home Improvement Programme 2 (HIP 2). Additionally, there is also the Voluntary Early Redevelopment Scheme (VERS) that the government has announced to help owners of these ageing flats unlock their flat’s value. These schemes not only help improve the liveability of these older flats over time but also ensure we won’t be stuck with an asset that cannot be realised.

While we should do our own due diligence before making any property purchase, financing older flats may be tricky. That’s why having a good, trusted mortgage broker like our friends at RedBrick can give you peace of mind, knowing that you will always get the best rates out there and enjoy unparalleled service.

Simply fill in the contact form and an experienced Redbrick mortgage specialist will be in touch with you for a free and non-obligatory quote and consultation.

Listen to our podcast, where we have in-depth discussions on finance topics that matter to you.

Read the full article here